Agent vs Aggregator Best Way to Buy Insurance in India

Naveen Kr. Tiwari

6/13/2025

In India’s rapidly growing insurance landscape, one of the most common questions people ask is:

“Should I buy insurance through an agent, an online aggregator, or directly from the insurance company?”

Whether you’re buying health, motor, life, or travel insurance, your buying experience—and satisfaction—can vary significantly depending on the channel you choose.

Drawing from my years of experience in the Indian insurance industry—working across underwriting, claims, and sales—I’ve seen the pros and cons of each channel from the inside out. Here’s an honest, easy-to-understand comparison to help you decide what’s right for you.

1. Buying Insurance via an Agent

Best For: Personal advice, senior citizens, complex needs, rural markets

Pros:

Human guidance: You get personalized advice tailored to your family’s needs.

Claims support: A good agent can help you during tough times like hospitalization or vehicle damage.

Relationship-driven: Agents often stay in touch for renewals or policy changes.

Cons:

Limited options: Most agents are tied to one or two companies.

Pricing may be slightly higher due to commission.

Sometimes over-selling or under-disclosing product limitations.

Best For: Those who value trust and personal relationships over self-research.

2. Buying via Aggregators (PolicyBazaar, Coverfox, etc.)

Best For: Comparison shopping, young and tech-savvy users, those who want to explore all options

Pros:

Multiple quotes in one place

Easy comparisons of features, premiums, and claim settlement ratios

Discounts and offers, especially on motor and health policies

Some provide pre-sales support via chat/call

Cons:

Post-sale service is often weak

Too many options can confuse new buyers

May receive spam calls after inquiries

Limited customization; not ideal for complex family or business needs

Best For: Internet-savvy individuals comfortable buying after some self-research.

3. Buying Direct from the Insurance Company Website

Best For: Simple policies, renewals, or brand-loyal customers

Pros:

Lowest premiums (sometimes no agent/aggregator fee)

Direct communication with insurer

Quick and secure digital purchase

Cons:

No third-party help if things go wrong

No one to explain hidden clauses

Can miss better deals on other platforms

Best For: Repeat buyers who already understand what they want.

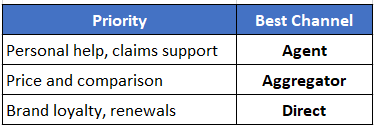

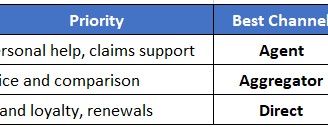

So, Which One Should You Choose?

There’s no universal winner—it depends on your priorities

Pro Tip (From My Experience)

Many buyers trust aggregators for the initial quote, but still buy through agents for post-sales support. Others do the reverse. The smartest approach is:

Compare via aggregators → Discuss with a trusted agent (if available) → Buy from the channel that gives you peace of mind.

Final Thoughts

At TheFinPulse, our goal is to simplify the insurance maze. Whether you’re protecting your health, life, car, or travel plans, the way you buy insurance matters as much as what you buy. Stay informed, stay covered.

Got questions? Drop them in the comments or ask me on Quora. I answer every genuine query.